Check back soon

Once posts are published, you’ll see them here.

We want to be bullish. We love to be bullish. It feels good when stocks are heading higher. Alas our discouragement this week when we started to recognize that perhaps we will not be getting our famed Santa Claus Rally this year. True the year before a presidential election is almost always the strongest part of the four year cycle. True the odds of a healthy fourth quarter stock advancement after a greater than 10% market drop in the third quarter sits at around a 90% probability. True our economic data as of late has all but taken the notion of a double dip recession out of the picture.

Fear not true believers, we continue to anticipate a market rally on the horizon that could take the S&P 500 higher by 25% to $1520 in the coming twelve months.

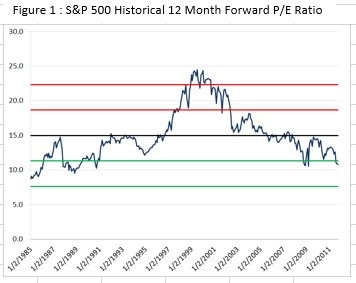

Fundamentally, we are close to getting significant buy signals. Analysts are forecasting the components of the S&P 500 index to report an aggregate $106 in the coming twelve months putting the earnings yield at 8.6% (or 11.7 twelve-month forward P/E ratio). Expected calendarized earnings growth for the index is 12%, tracking below the average 18% and the anemic ten-year treasury yield has been tracking around 2% for several weeks. By taking these measures into account, our belief is that the market has already priced in much of the current and expected market turmoil that has been reported over the last several weeks.

Barring an unknown event, such as a terrorist attack, natural disaster or the unlikely dissolution of the eurozone, our opinion is one of bullishness. With the market trading near 11.6x forward earnings, (the level associated with fear) investors are still shell-shocked from the massive shellacking taken in 2008 and took very little time to decide to run for the exits this time around. The twelve-month forward earnings forecast have come down approximately $2 from $108 in early September and earnings growth expectations have fallen from 20.9% in June to 12.0% today.

This indicates to us that much of the market turmoil has been worked into the existing forecasts. Once investors tolerance for risk increases, they will have the choice of remaining in treasuries yielding approximately 2% or moving cash into equities potentially yielding 8%. In search for greater returns, we are anticipating a rotation out of treasuries and into equities in the coming year.

While we are enthusiastic about the coming market prospects, one needs to be judicious in their analysis as to when to pull the proverbial trigger and get aggressive behind ones strategy. Our strategy has been one of caution over the past several weeks and months. We are building positions in stocks that we think will lead the rally when it eventually takes hold while maintaining our downside and hedged positions. There have been numerous events this past week that has given us pause as to the likelihood of this rally starting in the very near future.

We have surveyed five market conditions this week that we have determined needs to exhibit substantial improvement before we take any further bullish action. These conditions include; unusual activity coming from the Volatility Index (VIX), deteriorating market technicals, relative under-performance of the NASDAQ compared to the S&P 500, unproductive sector rotation and of course the on-going saga that is the European debt crisis.

Bottom line: There is a tremendous market rebound that is on the near-term horizon. We are positioning ourselves to best take advantage of this move. The challenging part of this entire plan is to know when to move solidly into the market. We will interpret our models to the best of our ability and document in this letter our strategy over time.

Market Volatility Index

We have been observing a breakdown in the correlated relative volatility between the Volatility Index (VIX) and the S&P 500 (SPX) over the last few weeks. By examining these trends and trends in the Put/Call ratio that has averaged 1.13 over the past 90 days compared to 0.81 long-term average, it is obvious market participants are trepidatious about entering the market.

In figure 2, the gray line represents the correlation between VIX / SPX volatility. One can see that when this correlation breaks down (rises closer to zero), as it has been since late March 2011, the stock market tends to head lower.

This breakdown in correlated relative volatility can start to reverse at any time, but for now it continues to head higher. The model currently registers 4.08. The upper probability band, which is one standard deviation from the historical mean, is 2.72. If that is the level that we are on pace for, then there would certainly be additional downside to this market.

This breakdown in the VIX/SPX relationship will also help explain why our VIX behavioral model (which represents 1/6th of our master behavioral model) has been on the rise without a corresponding rise of equal magnitude in the general market. From early October through Friday, both the trend and trigger line have risen from “extreme panic” to “rational market”.

Bottom Line: We would like to see correlated relative volatility between the VIX and SPX improve before we take aggressive long positions.

Range-Bound Markets

Last week we opined that a strong move in the S&P 500 above its 200 day moving average would be a desired signal for us to take a further bullish stance. Of course this move would need to be accompanied by robust volume. Needless to say, we did not get that action last week and, while typically fostering our investment thesis around quantitative methods, it does not take a master market technician to realize the equity markets are amply displaying unhealthy signals.

For one, there is a narrowing channel that the SPX seems to be bound to. This range seems to be somewhere between 1200 and 1260 (two red lines in figure). Interestingly enough, that upper channel seems to abut the 200 day moving average. We still hold the view that a breakout above this moving average, on higher than average volume will be a positive development for the market.

What’s worse, the 50 day moving average crossed the 20 day to the downside and all week the 50 day moving average (which is still upward sloping) has acted as intraday resistance while the downward sloping 20 day moving average has been acting as resistance at the close. Several times during the week, the market opened higher only to be soldoff towards the latter part of the trading day. Again, we are not claiming to be master market technicians, but these trends are enough to debilitate even the most earnest of traders.

Bottom Line: Investors don’t seem energized about the market right now and we will remain as market neutral as possible until we see the SPX break this narrow channel that has developed. If we break higher on volume, we are ready to get aggressive to the upside. If, on the other hand the SPX deteriorates beyond that bottom channel, then we will need to readdress our tactical strategy and perhaps take a short bias to the market.

NASDAQ relative under-performance

We continually look for clues as to market direction and guidance on how to proceed. One unsettling trend recently has been the relative under-performance of the NASDAQ relative to the SPX. It would appear the general pattern over the past week has been one of early enthusiasm that eventually degenerates into malaise over the trading day. The NASDAQ has been the index that has lead on the way down.

Figure 6 compares the performance of the two indices. When the slope of the two lines are heading lower, that means the NASDAQ is under-performing the SPX and we will remain in a market down trend. Clearly the slope of both the trigger and trend line are heading lower indicating further pressure on the market.

The only welcome bit of data from this model is that it is quickly approaching 2.0 standard deviations from the mean for both lines. That would indicate the relative under-performance of the NASDAQ may be short lived. Typically these lines do not stay below that outer band for long.

Bottom Line: We require the NASDAQ to exhibit dominant price performance relative to the SPX before we commit to further long biases.

Sector Rotation

Last week we were encouraged by the price performance of the individual sectors that embody the S&P 500. We have been tracking cyclical versus defensive sectors. With the resurgence of cyclical sectors as relative out-performers, we were compelled to increase our exposure to those names that would lead any perceived rally on the horizon and appreciate in price as the economy grew. We considered this trend to be preliminary evidence that a year-end rally would actually occur. That did not turn out as we had hoped and we have seen a complete reversal of that trend this past week.

Figure 7 shows our cyclical / defensive index. This simply compares the price performance to those sectors considered cyclical to those considered defensive. A few weeks ago the trigger line in this model started higher and pierced the trend line to the upside. We considered this a very positive development at the time. Since then, there has been a complete lapse in that relationship as both the trigger and trend line started heading aggressively south.

This indicates those investors that are buying US equities are choosing to purchase names in such defensive sectors as Health Care, Consumer Staples, and Utilities. With these sectors outperforming all other sectors, on cannot imagine a sustained rally.

Surveying sector performance on a weekly basis, this trend is evident in last week’s results. The best performing sectors have been Health Care, Utilities and Consumer Staples last week. The worst performing sectors include Energy, Materials and Information Technology.

Bottom Line: We need to see a strong and steady rotation back into those sectors that will lead the market higher. Until that trend is unambiguous, we will continue to wait before going risk on.

Euro Crisis continued

While we had high expectations towards a debt crisis solution, it would appear the results from last week’s EU summit provided little comfort to investors. Yields on European sovereign debt did ease somewhat, but not nearly enough to infer purchasers of this debt thought the crisis was nearing a genuine solution.

Looking at the change in yields on European sovereign debt dating back to the first quarter of this year, one can see the pronounced shift to safety as several European economies started to crumble. Yields on the German ten year has fallen 43% to yield 1.9% compared to 3.3% at the start of the year. The United States 10 year treasury has fallen 47% to year 1.8% versus 3.5% at the start of the year. These yields continue lower even after the proposed EU solution. When the eurozone finally figures out a tangible solution to its debt problem, we will know it when yields on these instruments start to head higher. It would also indicate a higher tolerance for risk that would be beneficial to the stock market. Until that happens, we would expect lackluster stock performance. The language and opinions that have been articulated since the summit have been extremely interesting, insightful and alarming. Talk of economic catastrophe, agitprop and the Fourth Reich can have one second guessing the very existence of European as we know it today. While we are not that the camp that all things European are doomed, we recognize the potential hardships that lay ahead for Europe. In all, there has not been much written this past week that exhumes confidence in the political leadership in Europe.

“Governments on both sides of the Atlantic are trying to use the crisis to grow rather than shrink. News of Europe's fiscal incompetence abounds, but Washington had no budget at all in 2010 or 2011 and the federal deficit grew at record pace. President Obama sailed through 2011 without any significant spending cuts or government downsizing…To win elections, politicians have promised practically endless government spending and covered up the cost, leaving generations of taxpayers obligated to pay off the debt. That's wrong, but neither the U.S. nor Europe has a plan to stop it. A first step would be to use more effective debt and deficit limits to force governments to spend less and end the debt cycle.” And the Crisis Winner Is? Government – David Malpass, Wall Street Journal opinion , 12/16/11.

“Or so it seems from European newspapers, which now refer bitterly to a "Fourth Reich" and arrogant new Nazi "Gauleiters" who dictate terms to their European subordinates. Popular cartoons depict Germans with stiff-arm salutes and swastikas, establishing new rules of behavior for supposedly inferior peoples.

Millions of terrified Italians, Spaniards, Greeks, Portuguese and other Europeans are pouring their savings into German banks at the rate of $15 billion a month. A thumbs up or thumbs down from the eurorich Merkel now determines whether European countries will limp ahead with new Germanbacked loans or default and see their standard of living regress to that of a halfcentury ago…

Behind all the EU's 11th-hour gobbledygook, Germany's new European order is clear: If you wish to live like a German, then you must work and save like a German.

Take it or leave it.” How Grand Dream Ended In A German Protectorate – Victor Davis Hanson, IBD opinion, 12/16/11.

“The recent eurozone summit was a double failure. It failed to achieve the increased European political integration that was the primary goal of German Chancellor Angela Merkel and the other European political leaders. And it failed to improve the outlook for eurozone sovereign bonds because those politicians continued to insist that only a fiscal union and political integration could limit the interest rates on sovereign debt…

The MerkelSarkozy team should recognize that they have been on the wrong track. Europe needs country-bycountry fiscal reforms and not a renewed push for a fiscal union and political integration.” The Euro Zone’s Double Failure – Martin Feldstein, Wall Street Journal opinion, 12/15/11.

“What happens if the euro collapses? A euro area breakup, even a partial one involving the exit of one or more fiscally and competitively weak countries, would be chaotic. A full or comprehensive breakup, with the euro area splintering into a Greater Deutschmark zone and about 10 national currencies would create pandemonium. It would not be a planned, orderly, gradual unwinding of existing political, economic and legal commitments. Exit, partial or full, would likely be precipitated by disorderly sovereign defaults in the fiscally and competitively weak member states, whose currencies would weaken dramatically and whose banks would fail. If Spain and Italy were to exit, there would be a collapse of systemically important financial institutions throughout the European Union and North America and years of global depression…

Even if a break-up of the eurozone does not destroy the EU completely and precipitate the kind of conflicts that disfigured the continent in the past, the case for keeping the show on the road seems rather robust.” The Terrible Consequences of a Eurozone Collapse Willem Buiter, Financial Times opinion, 12/7/11.

“So Europe is trapped in Purgatory. What’s economically sensible is politically treacherous, and what’s politically sensible is economically treacherous. Moreover, the euro’s promise has been turned on its head.” The Purgatory That Is Europe – Robert J. Samuelson, IBD opinion, 12/15/11.

“One answer is playing out now as a Greek tragedy: You have a depression. And if neither monetary stimulus, fiscal stimulus, nor currency depreciation is possible, when does this depression end? It may take quite a while. Real GDP in Greece is already down about 12% and still falling—which is why you've heard so much talk about Greece leaving the euro. Of course, what happened in Greece didn't stay in Greece. Markets started turning on the other wounded antelopes in the European herd: Portugal, Ireland, Spain, Italy and so on…

Europe continues to try to stave off disaster. In the latest summit agreement, reached last Friday, all 17 eurozone countries, plus several others, pledged to pursue fiscal discipline—with tighter enforcement than previously. But that agreement is more about forestalling future crises than curing the present one. And fiscal austerity all over Europe, if it comes, will deepen the recession. So we hold our breath and await salvation from the European Central Bank (ECB) in the form of potentially massive bond purchases.” The Euro Zone’s German Crisis Alan S. Blinder, Wall Street Journal opinion, 12/13/11.

“The Moody's report signals that Europe's crisis has entered a new, more dangerous phase. People are openly discussing outcomes that once seemed unthinkable: a breakup of the euro area; mass bank failures.

Writing in Tuesday's Financial Times, Polish Foreign Minister Radoslaw Sikorski warned:

"The breakup of the euro zone would be a crisis of apocalyptic proportions, going beyond our financial system. Once the logic of 'each man for himself' takes hold, can we really trust everyone to act in a communitarian way and resist the temptation to settle scores in other areas, such as trade?"” How Close Has Europe Drawn To The Abyss? – Robert J. Samuelson, IBD opinion, 11/30/11.

“In the long-term, more discipline and coordination and more financial transparency are good things. But a pact that binds all members to more austerity in a time of recession is exactly what Europe does not need right now. The agreement will also increase the money available for future bailouts. But the amounts are still far too small to persuade investors that Europe is prepared to back up much larger economies like Italy and Spain. And it still leaves the euro zone without a lender of last resort, like America’s Federal Reserve, to defend vulnerable countries and banks from market panic…

Europe has learned the hard way that sustainable monetary union requires better coordination of national fiscal policies. Greece wrecked its finances by overspending, undertaxing and falsely reporting its budget numbers. But major leaders, especially Chancellor Angela Merkel of Germany, still refuse to acknowledge that coordination isn’t enough.” Europe’s Latest Try – New York Times opinion, 12/10/11.

Our hopes are for a clear and uncompromising solution that will not only curtail the panic stricken volatility that the markets of all instruments have had to suffer, but offer long-term stability that can be a model for other nations that may face similar circumstances. We are in agreement that there needs to be concrete and serious preconditions before the real work starts. Countries that have become addicted to overspending need to first admit there is a problem and commit to serious reform, even if it means taking a subservient role to a larger fiscal authority. In lock step with this commitment on the part of European leaders, the ECB must take a more active role immediately without violating their charter to support those European nations that face budget shortfalls. This can be done by working directly with the IMF. The global economy will be willing to bear some of the liability if it is shown that those countries with fiscal problems have taken serious steps towards fiscal reform.

Once this phase is complete and the markets are stabilized, then there needs to be serious conversation about centralized fiscal policy. This may take changes in EU and ECB law, but in the end it will be necessary to avoid another crisis. While we are not on the centralized regulation camp, if the intention is to continue to entertain a single currency and centralized monetary policy, then centralized fiscal policy is in order. Creating a mechanism whereby a central fiscal entity can approve and support an individual nation’s budgetary needs and growth initiatives will restore confidence in the European economic model.

Having a complete handle on the budgetary needs of member nations, a single euro-bond can be issued at attractive rates. With reduced cost of capital to support fiscal reform, this will give Europe the time it needs to restructure and regroup while putting pro-growth initiates in place.

Joseph S. Kalinowski, CFA

Comments