Check back soon

Once posts are published, you’ll see them here.

It appears we had quite a bit of news coming from Europe over the weekend and this coming week will offer additional data points for investors to digest.

The big news from Greece is that the country’s center-right New Democracy party was victorious in the elections, besting the far-left Syriza party. Markets and global central banks had feared that if Syriza had walked away victorious, the process of Greece’s exit from the euro would have been set in motion. The victory of the New Democracy party has assured markets that Greece will continue to attempt to remain in the euro, as opposed to an abrupt and messy exit.

In France, newly elected President Hollande’s Socialist government secured a clear majority in the final round of France’s parliamentary elections. There appears to be anti-austerity sentiment that is sweeping southern Europe and with the win by the Socialist party, one will expect this movement to accelerate putting increased pressure on Germany’s Merkel to soften her stance on budget cuts. A move she has been unwilling to entertain in the face of increased bail-out needs from several European nations.

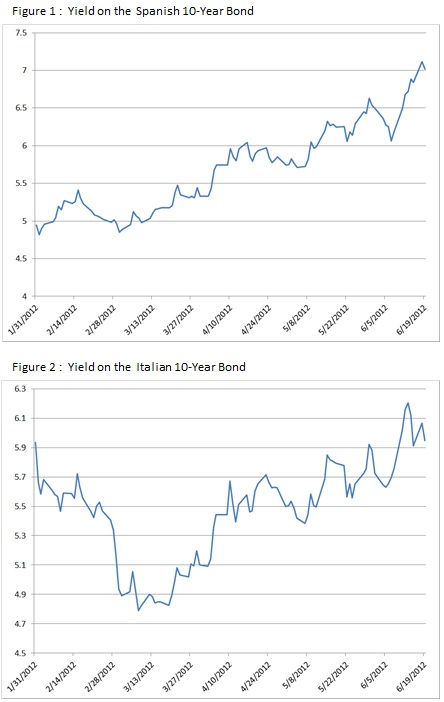

Spain received a commitment last week for one billion euros ($125 billion) to shore up a possible banking crises looming on the horizon. While initially applauded by the market, sentiment soon soured. Spanish yields on the ten year sovereign debt soared to new heights on concerns that this type of borrowing by Spain would drive their debts through the roof with the side-effects of this treatment actually exacerbating the disease.

On the other side of the coin, perhaps the bond vigilantes are assuming that $125 billion (yes billion with a B) isn’t enough money to stave off the coming catastrophe. In any case, borrowing costs for Spain is now sitting at its highest point since this crisis began.

Yields on the Spanish ten-year and firmly above 7%, a level certainly associated with disaster, the spread between it and the German 10-year is roughly 550 basis points and borrowing costs for Spain have risen by 30% over the past year. Given the stats, this is hardly a ringing vote of confidence by investors.

Italy has taken their message public that it is NOT next in line for a bailout. Given all the hoopla from Spain, Italian Prime Minister Mario Monte has publically stressed that Italy is not seeking help from the Eurozone and their issues are largely contained. Once again, the markets just don’t buying it. Yields on the Italian ten-year launched past 6% recently and is sitting on that mark as of the time of this writing.

The Italians have been raising taxes in order to attempt to 1) close their budget deficit and 2) stimulate growth by increased public sector spending. Last week we commented on this strategy (currently promoted by the Obama administration) and expressed our belief that this is a wrong policy path for a nation that is struggling economically.

“Data released last week showed that value-added-tax revenue fell over the past 12 months, even though—sorry, make that because—Rome raised the rate to 21% last year. The VAT rate is due to rise to 23% in October. A new property tax on primary residences kicks in next week…Italians continue to pay a top marginal income-tax rate of 43% that kicks in at €75,000 and rises to 46% for those making more than €300,000. That might help explain why tax evasion is endemic in Italy, and why an astonishing 27.4% of Italian GDP is off the books, according to a recent estimate by an Italian Central Bank official.” Italy’s Reform Stall – Wall Street Journal opinion – 6/14/12.

Perhaps we’ll get more clarity on the potential solutions from this week’s G20 meeting in Mexico, but we highly doubt it. What we will get is more of the same “why the other guys plan won’t work” as opposed to a breakthrough resolution.

That said, our hopes are for a clear and uncompromising solution that will not only curtail the panic stricken volatility that the markets of all instruments have had to suffer, but offer long-term stability solutions to avoid similar crises going forward. We are in agreement that there needs to be concrete and serious preconditions before the real work starts. Countries that have become addicted to overspending need to first admit there is a problem and commit to serious reform, even if it means taking a subservient role to a larger fiscal authority. In lock step with this commitment on the part of European leaders, the ECB must take a more active role immediately without violating their charter to support those European nations that face budget shortfalls. This can be done by working directly with the IMF. The global economy will be willing to bear some of the liability if it is shown that those countries with fiscal problems have taken serious steps towards fiscal reform.

Once this phase is complete and the markets are stabilized, then there needs to be serious conversation about centralized fiscal policy. This may take changes in EU and ECB law, but in the end it will be necessary to avoid another crisis. While we are not in the centralized regulation camp, if the intention is to continue to entertain a single currency and centralized monetary policy, then centralized fiscal policy is in order. Creating a mechanism whereby a central fiscal entity can approve and support an individual nation’s budgetary needs AND growth initiatives will restore confidence in the European economic model.

Having a complete handle on the budgetary needs of member nations, a single euro-bond can be issued at attractive rates. With reduced cost of capital to support fiscal reform, this will give Europe the time it needs to restructure and regroup while putting pro-growth initiates in place.

The alternative may be anyone’s guess.

“The Bundesbank said there should be no banking union until there is a fiscal union. Angela Merkel said that there should be no fiscal union until there is political union. And François Hollande said that there should be no political union until there is a banking union.

What if there is no deal or another fudge? In that case, I would expect Italy and Spain to leave the eurozone. If a banking union is a necessary prequisite for a monetary union, and you are told that a banking union is politically unacceptable, then one must sadly conclude that the monetary union is unfeasible. I do not say this lightly. A break-up would be catastrophic.

In the absence of a deal next week, I would expect to see an acceleration of a slow-motion bank run. Why should citizens leave their money in their local banks, when foreign investors are pulling out and when even the EU is making preparations to impose capital controls? Market interest rates will rise further and it will only be a matter of time before both Italy and Spain are cut off from market funding.

If Italy and Spain were to leave the eurozone, they would probably also default on their foreign debt. Such an act would probably cause the European financial system to collapse – something that would ultimately reverberate in Italy and Spain, too. But the irony is that an Italian or Spanish exit would probably end up hurting France and Germany more than it would hurt Italy or Spain.” What happens if Angela Merkel does get her way – Wolfgang Munchau – Financial Times – 6/18/12.

Geez, he must be a great time at a party.

European leaders have taken quite a bit of time to figure out this situation, as is justified given the severity and magnitude of the crisis. But the markets’ patience has worn thin and gone are the days of short-term relief and leeway every time European leaders plug their finger into another hole in the leaking dike. The markets want results out of Europe and countries like Spain and Italy are currently feeling that wrath.

The Fed meets this week.

Pardon the nostalgia, but recall the days when the stock market would rally on positive economic news. Lately the market has taken an opposite view and now moves higher on weaker than expected economic releases. This is partly because of an increased expectation that the Federal Reserve will take additional monetary policy maneuvers to promote growth. They are meeting this week. Should something be said that promotes asset appreciation, we are prepared to increase our long exposure knowing that a rally can be hiding anywhere amongst the most sanguine of market moods.

Our behavioral model has picked up on this changing sentiment and we have been slowly deploying assets back into U.S. equities. As our clients may have recognized, after being largely sidelined for the past few weeks and months, we have started to buy back in, much to the benefit to our investors as the month of June is shaping up to be a pretty good month.

When the market seems its darkest and blood lines Wall Street, is the time to consider going against the grain and buy when others are scrambling for the exits.

Joseph S. Kalinowski, CFA

Comments