Check back soon

Once posts are published, you’ll see them here.

The word out of Jackson Hole is that the Fed is prepared to raise rates once or twice this year depending largely on the economic data over the next several weeks and months. The markets are placing a 36% chance of a rate hike during the September meeting and 59% chance of a hike in December.

We’re a bit skeptical if the U.S. economy and the stock market could easily absorb these expected hikes. The economic data that we are viewing doesn’t appear all that encouraging.

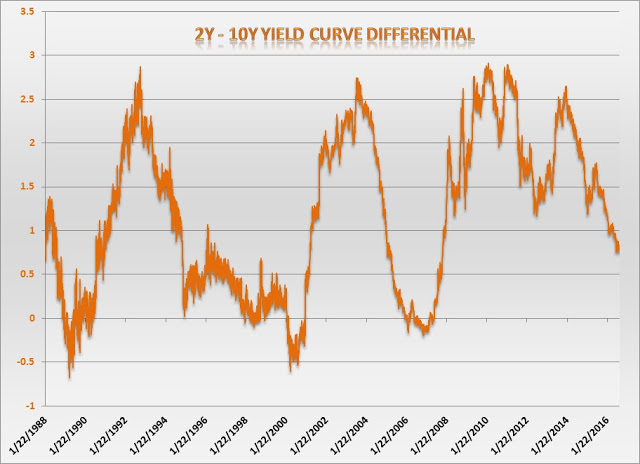

The flattening yield curve (two and ten-year yield) give us cause for concern.

NFIB small business optimism has been improving somewhat but remains below trend.

The year-over-year growth rates of real personal income, non-farm payrolls, retail sales and industrial production all seem to be trending below average.

We like to aggregate the manufacturing indices into one chart. Our reading includes; ISM, Chicago, Dallas, Richmond, Philadelphia and New York manufacturing surveys. This measure has been trending below average for quite some time.

Truck tonnage is still positive year-over-year but trending lower and total year-over-year rail shipments remain negative. We have always considered the movement of “stuff” as a great leading indicator of economic strength so we’re not very excited about a strong economic rebound on the horizon.

The Conference Board Leading Economic Index is still positive year-over-year but heading in the wrong direction.

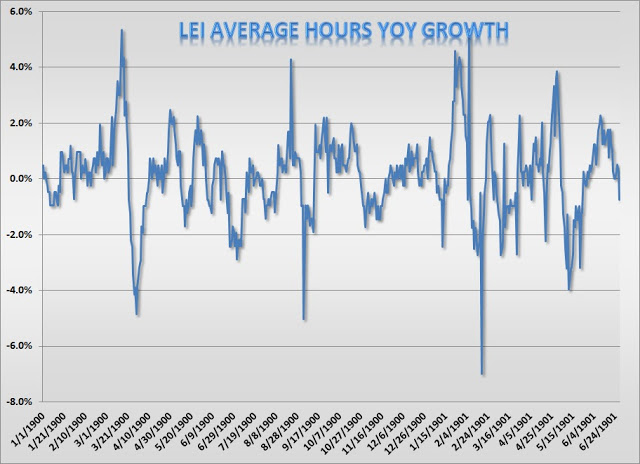

LEI year-over-year growth in building permits, average hours worked, credit index and new orders all seem to be weakening as of late.

The Atlanta Fed’s GDPNow is forecasting 3.5% GDP growth in the third quarter. This reading has been fairly accurate over the past year and we’ll be watching it closely. The New York Fed’s Staff Nowcast Report is estimating 2.8% for 3Q GDP.

Here is our Thesis. The economic numbers have been lackluster over the past several quarters and we are not seeing much of an improvement recently. Perhaps the expectations are too high and that is reflected in the market. Notice the Financials and Technology are the two sectors that have supported the market over the past month.

As we mentioned in our last blog Defensive Positioning we are taking a defensive stance towards the market. We expect the month of September to be weak as has been the case historically.

Bottom Line: We are not in the camp that the economy is as strong as the Fed is projecting. That said we do not believe a recession is in the making currently. We anticipate a pullback in the market for September. We have taken an oversized cash position in our core portfolio heading into September and have been building defensive positions in our pair’s trading portfolio. We will stand ready to re-deploy capital on a pullback.

Joseph S. Kalinowski, CFA

Comments