Check back soon

Once posts are published, you’ll see them here.

At the time of this writing (5/29/18), the US equity markets are selling off aggressively as geo-political events in Europe take center-stage. Over Memorial Day weekend it has become apparently clear that Italy will hold fresh elections at some point later in the year. This type of political uncertainty within the Euro-Zone’s third-largest economy has sent shutters through the entire global financial markets, especially in light of the growing antiestablishment, Eurosceptic sentiment that has placed the 5-Star Movement as the largest political party in

Italian politics.

The 5-Star Movement won 222 out of 630 seats in Italy’s lower house of government during the March elections. This was an impressive showing to say the least, but well short of the ability to form its own government and after three months of attempting to form a coalition government with the Lega Nord, it appears that their alliance has been broken.

The rejection of Paolo Savona, the coalitions choice of finance minister by Italian President Sergio Mattarella has spooked the global markets. Another election brings about the possibility of greater support behind the 5-Star Movement which increases the chances of an Italian exit from the Euro. With Italy as the third-largest Euro-zone economy behind Germany and France, experts hypothesize the Euro experiment will come to an end without the support of Italy.

Italian Yields and Spreads

The Italian ten-year bond yield has spiked to almost 3% from a range of 1.7% to 1.8% just a few weeks ago.

German yields have come down aggressively as a result of a flight to safety move so thus the current spread between the German and Italian ten-year is a whopping 265 basis points, up from 130 to 150 bp over the past several weeks.

This marks the largest spread in nearly five years but nowhere near the levels during the 2011-2012 debt crisis. Should the market get further evidence of an upcoming election that could seemingly end the country’s Euro participation, we would expect these spreads to increase further with a significant breakdown of sovereign debt and quite possibly a banking crisis that spreads throughout Europe, eventually infecting the entire global economy.

As a consequence, the Euro is hitting five-month lows against the US Dollar and threatens to break support. It seems €1.21 to €1.22 to the dollar is key support and also represents a 50% Fibonacci retracement from the early 2017 lows.

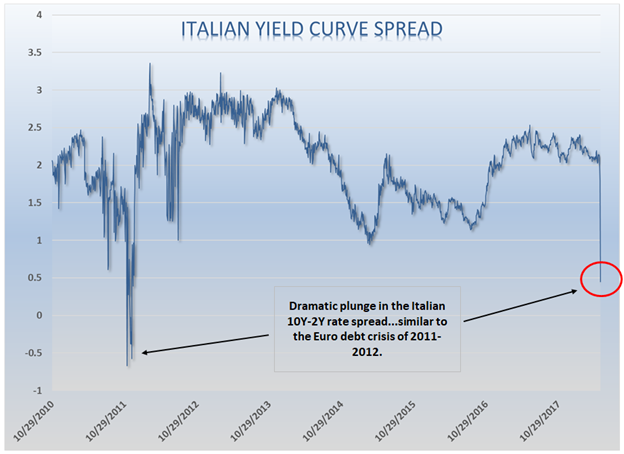

We will be watching the spread between the Italian two and ten-year yields for further insight as to the markets level of confidence regarding the Italian elections and overall economic growth. The sudden drop that we are seeing currently seems similar to the type of nervousness that was prevalent during the 2011-2012 banking crisis and does not bode well for the near-term outlook on equity prices, bonds and the Italian economy.

Italian Equities

The Italian equity market as measured by iShares MSCI Italy Capped ETF (EWI) has dropped significantly over the past several days and it sitting on the 38.2% Fibonacci retracement from the lows in 2016. Momentum as measured by the MACD is displaying significant deterioration indicating a test of the 50% Fibonacci retracement level. This would equate to a 21% selloff of Italian equities this year, placing that particular market in bear territory.

Italian Equities as a Buy

The valuation dynamic for the Italian ETF is starting to look compelling. Using the FTSE MIB Index as a fundamental guide (there is a strong correlation between the FTSE MIB Index and the EWI ETF of 97.3%), one could make the argument that if things workout with the geopolitical drama unfolding in Italy, there is an attractive investment opportunity in the making.

The FTSE MIB is expected to earn $1954 in the coming twelve months and is currently trading 10.9x forward earnings compared to an average of 13.5x over the last five years. This represents a 23% discount over the past few years. The long-term consensus forecast for earnings growth is currently 12.5%. Using these figures, one can expect an IRR of nearly 15% per year over the next five years.

Crisis Mode

If we were to enter crisis mode similar to that of 2011 and 2012, then we could see additional downside to the Italian markets. In the wake of the Euro crisis, Italian earnings expectations for the equity market dropped almost 35%. The market was at the time trading near 7.5x forward earnings at the worst. A 35% drop in today’s consensus forecasts would bring the EPS number down to $1270. At 7.5x that figure, Italian equities would be trading near $9525, down another 55% from today’s levels or roughly $13 per share for EWI. This would be the lowest levels for the ETF since the 2001-2002 recession and the 2008 Great Recession. This is clearly the worst-case scenario but not entirely inconceivable should Italy decide to leave the common currency.

We are looking for the Italian yield curve to stabilize and watching where final support will be on the stock charts. We’ll be monitoring the deterioration in earnings projections and subsequent adjustments higher. We will be closely studying the events and elections as they unfold. Once the geopolitical environment shows signs of improvement, we anticipate an appropriate investment entry at some point between today’s levels and our worst-case scenario.

Joseph S. Kalinowski, CFA

Comments